Inventory is a direct cost to the company, and it can hamper the company’s growth if not managed and evaluated properly. Inventory can be raw material, goods in production, or finished goods ready for sale. If the company does not know how much capital its current inventory holds, it cannot properly plan its future procurement and execute business operations. In short, the inventory valuation is the monetary value of unsold stocks at the point of reporting period, and depicts the overall health of the business. The business rule book suggests that keeping minimum inventory is in the best interest of the company.

Inventory valuation is done at the end of each financial year to figure out the cost of goods sold – which is to determine the company’s business gross profit and financial position. It’s also crucial from the point of filing taxes.

A wrong evaluation of inventory could drive business towards a dead-end. Besides that, investors consider inventories (current assets) for lending funds to the company. Business owners can evaluate the costs of the inventory accurately if they are managing them efficiently. In order to get clear visibility on the inventory and manage them efficiently, inventory management tools can be pretty helpful. Business owners can make inventory valuation more meaningful with an organized inventory management system and take benefits of inventory management software’s features.

What Are the Methods for Inventory Valuation?

There are three methods of Inventory Valuation.

- FIFO (First In, First Out): First in First out (FIFO) means the inventory that first enters the warehouse, and is sold out first. In this method, the cost of the oldest inventory (purchased first) is considered while evaluating inventory.

- LIFO (Last In, First Out): As the name indicates, “last in, first out,” the most recently purchased inventory is sold first. LIFO is generally used for inventory whose price varies frequently. U.S is the only country that allows LIFO as it follows the Generally Accepted Accounting Principle ( GAAP) rather than International Financial Reporting Standards (IFRS).

- Weighted Average Cost: The weighted average cost is used when the inventory items are so blended or identical to each other that it is difficult to assign to one particular cost. In this technique, the average cost of inventory is calculated by dividing the total cost of the inventories by the number of inventories still on the shelf. The weighted average cost falls somewhere between the oldest and newest inventory price. GAAP and IFRS both accept WAC.

How to Calculate Inventory Valuation?

The inventory price could vary during the entire year, and based on the business priority, the price is considered for inventory evaluation. There are three popular methods to calculate inventory valuation.

1. FIFO (First In, First Out) Valuation- This is a method where the value of the closing inventory can be easily calculated.Let’s assume that business buys televisions at regular intervals throughout the year. The rates of these televisions are different at different periods or months.

First purchase (Jan to July) – 10 televisions at $500

Second purchase (August to December) – 5 television at $600

Assume that total numbers of televisions that the store sold out are 7 out of 15 by the end of the year.

Accounting balance for COGS = (7 x $500) = $3500. (Televisions purchased first are sold first at $500)

At the end of the year 8 televisions were left, 3 from the first purchase (Jan to July) at $500 each, and 5 from the second purchase (August to December) at $600 each.

So the accounting balance of the inventory account as per FIFO = (3 televisions X $500) + (5 televisions X $600) = $4500.

2. LIFO (Last In, First Out) Valuation-

LIFO is opposite to FIFO.

First purchase (Jan to July) – 10 televisions at $500

Second purchase (August to December) – 5 television at $600

Let’s assume that the store sold 3 televisions by the end of the year:

Accounting balance for COGS = (3X $600) = $1800. (Televisions purchased recently are sold first at $600)

At the end of the year, 12 televisions were left, 2 from the recent purchase (August to December) at $600, and 10 from the first purchase (Jan to July) at $500 each.

So the accounting balance of the inventory account as per LIFO = (2 televisions X $600) + (10 televisions X $500) = $6200.

3. Weighted Average Cost ( WAC)

In the weight average cost method, the business has to consider the average cost of the televisions.

First purchase (Jan to July) – 10 televisions at $500

Second purchase (August to December) – 5 television at $600

Total televisions purchased 15 at cost $ $500 and $600. So the total amount invested in procuring 15 televisions is $5000 (10X$500) +$3000 (5 X $600)= $8000

So the average weighted average cost would be $8000 divided by 15 televisions which is $533.

After selling 12 televisions:

Accounting balance for COGS = (12X $533) = $6396

3 televisions were left unsold:

Accounting balance for inventory account with WAC= (3 X $533) = $1599.

Which Inventory Valuation Method Is Best for Your Business?

There is no one-size-fits-all when it comes to the inventory valuation method. The inventory valuation can vary based on the business type, financial goals, market condition, etc. However, FIFO is the most preferred method for inventory valuation; as such most companies try to sell the oldest product first. It is used to avoid the depreciation of the inventories. It is widely used when companies want to reflect a company’s growth and attract investors. It helps business owners to keep the Inventory costs high.

On the other hand, LIFO is ideal in inflation conditions. The inflation could be due to supply chain issues, product shortages, or a pandemic. With the LIFO technique, the company can note a drop in their net income but an increase in cash flow. Low net income means lower taxable income. However, LIFO is banned by IFRS globally apart from the USA. In short, if the goal is to assess the inventory cost, then FIFO is a better option, but if the company’s objective is to reduce the taxes, then they can go for LIFO (applicable in the USA only).

Whereas, if the business owners are dealing with a large volume of identical products, then they can opt for WAC. It requires less documentation and is easier to calculate the inventory cost. The manufacturing or agriculture sector often uses the WAC inventory valuation method.

Things to Consider While Selecting Inventory Valuation Method

Selecting the inventory valuation method is critical because an incorrect reporting of inventories can lead to accounting errors, and companies cannot make the right business decisions.

- Cash flow: While considering the inventory valuation method, business owners should evaluate how it impacts the business cash flow and how it would look in the next couple of years.

- Financial statement: Select inventory valuation method based on business priority; if the business demands to showcase higher net income, then choose the inventory valuation method accordingly.

- Stability: Various costs associated with the inventory valuation method are raw material, manufacturing costs, transportation, import duties, etc. These costs can change overnight, and it could affect the inventory valuation. So, it is recommended that business owners choose the inventory valuation method least affected by the change in these costs.

Conclusion

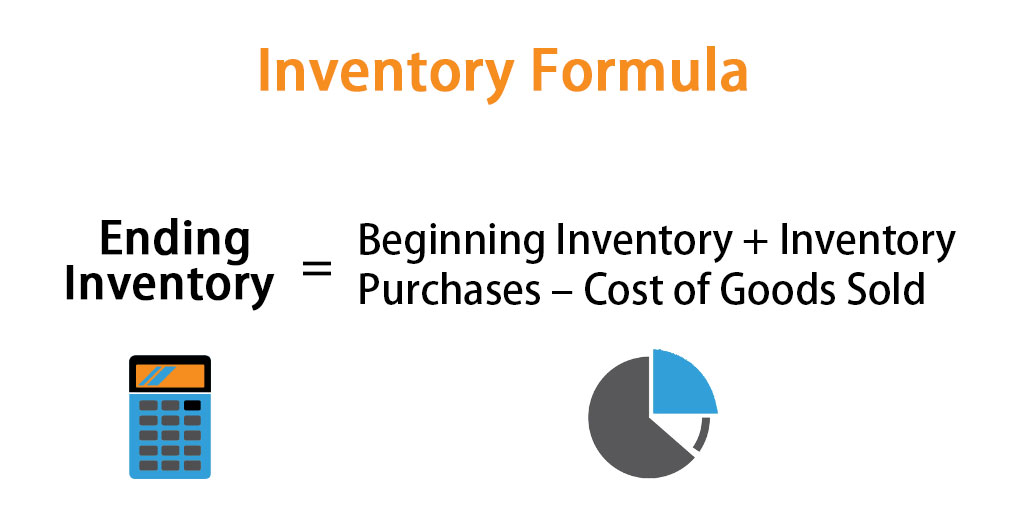

Inventory being the largest current asset for the company, it is essential to evaluate the costs associated with the inventory procurement, storage, and distribution. A periodic inventory system allows companies to conduct their Inventory valuation and understand the company’s fair financial position, to make critical business decisions, and attract investments. The selection of inventory valuation methods can have a massive impact on business planning, profitability, and taxes. Therefore, it is necessary for an organization to choose the right inventory evaluation method and accurately calculate the costs associated with inventory management.

Get connected with AppCloneScript to get updated information.